Through the Coronavirus Aid, Relief, and Economic Security (CARES) Act and the Paycheck Protection Program and Health Care Enhancement Act (PPPCHEA), the federal government allocated $178 billion in Provider Relief Fund (PRF) payments to support healthcare providers through the COVID-19 pandemic. Because the money comes from the federal government—it is being distributed by the Department of Health and Human Services (HHS)—those accepting the money, including nonprofits, could be subject to Single Audit requirements, as outlined in the regulations at 45 CFR 75 Subpart F. Requirements for a Single Audit are triggered when an organization expends, in aggregate, $750,000 or more of federal funds in a year.

What you should know about the Single Audit Requirement:

• The federal government specifies that independent auditors should be engaged to determine whether the financial statements, including a schedule of expenditures of federal awards (SEFA), are presented fairly.

• In conducting a Single Audit, auditors look to ensure the entity complied with the terms and conditions of the federal award as well as test the internal controls of the organization relevant to compliance.

• The auditor you select should be specifically trained for and capable of conducting a Single Audit. Not all auditors or auditing firms perform Single Audits.

• The Office of Management and Budget’s (OMB) Compliance Supplement specifies the PRF reporting requirements.

• The entity, with assistance from the auditor, will be required to submit the audit through the Federal Audit Clearinghouse. The data will be analyzed to determine whether the money has been used as intended.

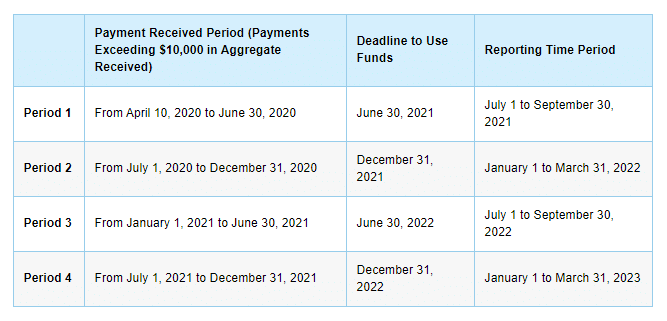

• Until recently, many healthcare providers were uncertain as to how to report their Provider Relief Fund expenditures. Financial statements for calendar-year organizations could not be issued because there was no definitive guidance or mechanism for reporting on their uses of the funds until July 1, 2021.

• The new reporting guidance includes hard deadlines for the use of the funds and reporting through both the PRF reporting portal and on the entity’s SEFA. However, entities are reporting expenditures in a manner they are not accustomed to. Audits for a particular year typically cover expenditures made during that year. But entities spending part or all of their funds in the year they receive them will not report on those expenditures until the following year (see chart below).

• HHS had indicated the deadlines to report are firm; there are no extensions.

What you should do now:

• Start gathering the information you will need, as indicated in the HHS reporting portal, including a wide range of demographic and financial information.

• Draft your SEFA and determine if you require a Single Audit.

• Document key positions regarding the calculations of lost revenue and qualifications of expenses in relation to PRF compliance requirements.

• Engage an independent auditor with the proper training and experience, one who is qualified and practiced at doing a Single Audit.

We are here to help. Call us at 724-934-5300; or email me at dmastropietro@hbkcpa.com.

Speak to one of our professionals about your organizational needs

"*" indicates required fields